IMIB Journal of Innovation and Management

Search

Search

Meraj Inamdar1, Ranjith Krishnan1 and Shweta Mehrotra2

1National Institute of Securities Markets (NISM), Raigad, Near Navi Mumbai, Maharashtra, India

2Institute of Public Enterprise, Hyderabad, Telangana, India

Creative Commons Non Commercial CC BY-NC: This article is distributed under the terms of the Creative Commons Attribution-NonCommercial 4.0 License (http://www.creativecommons.org/licenses/by-nc/4.0/) which permits non-Commercial use, reproduction and distribution of the work without further permission provided the original work is attributed.

This study attempts to perform content analysis, which is based on specific paradigms of unobtrusive research techniques, including conceptual and document analysis of the dividend distribution policies of the top 200 listed companies by market capitalisation to assess whether the policies enunciated by the companies align with the parameters suggested in the SEBI regulation. To conduct a content analysis, the authors use a three-step methodology to collect the dividend distribution policy documents and thus evaluate their content. First, we revisited the regulatory framework for the dividend policy and the provisions laid down by the regulators. The necessary information pertaining to the divided policy as per the legislations was retrieved from the policy documents and categorised further for the analysis. Finally, the collected information in the form of a document as per different categories was used as primary data for the content analysis. Our analysis found that dividends declared by companies were largely guided by the board’s long-term strategy. Further, looking from the investors’ perspective, having in place a dividend distribution policy for companies has probably not addressed their needs.

Dividend policy, retained earnings, SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015, dividend payout

Introduction

The distribution of dividends by firms remains a quandary for finance researchers because of its implications on the various aspects of a corporation and its stakeholders (Black, 1976). Indeed, the relationship between dividend policy and investment decisions has been a subject of extensive study in the field of finance (Fama, 1974). The literature on ownership and dividend policy in the corporate sector is vast and varied. One early study on the topic is the work of Modigliani and Miller (1958), who developed the concept of the ‘cost of capital’ and its implications for corporate investment and dividend decisions. Their work laid the foundation for much of the subsequent research in this area. Black (1976) famously referred to the ‘dividend puzzle’—the observation that firms often pay dividends even though they could potentially use the cash for reinvestment opportunities. Lintner’s work in 1956 indeed made significant contributions to the understanding of dividend policy. This puzzle has been the subject of much research, with Lintner (1956) offering one of the first elucidations for the payment of dividends through his ‘bird in the hand’ theory, which suggests that investors prefer the certainty of a dividend payment to the uncertain future value of retained earnings. Researchers such as Franco Modigliani, Merton Miller and John Gordon, known for their seminal work in dividend policy, provide different views on dividend policy and the other matters allied thereof. The traditional approach propounded by Modigliani and Miller (1958) views dividend decision as irrelevant of firm value. Contrary to this, the modern scholars view dividend policy as important decisions impacting the value of firms (Gordon, 1963). One theory advocates the payment of high dividends, and another school of thought opposes it considering the risk-taking ability of the investors. The significance and implication of a dividend policy cannot be overlooked.

It is more pertinent to an economy like India, where concentrated ownership structure is a predominant shareholding pattern (Balasubramanian & Anand, 2013; Chakrabarti et al., 2008; Claessens et al., 2002). Such type of shareholding pattern may have two implications. The principal block holders, as major shareholders, have a strong motivation to enhance shareholder value by addressing agency conflicts and aligning manager and shareholder interests (Bukart, 1997; Jensen & Meckling, 1976). Furthermore, it offers significant opportunities for large shareholders, particularly directors and promoters, to have increased incentives and control over a company’s financial decisions, particularly with regard to dividends. A well-defined and transparent dividend policy is crucial as it conveys positive signals to shareholders and reflects positive corporate performance. On the other hand, a lacking or vague dividend policy, or a failure to adhere to it during dividend declaration, negatively impacts the securities market by shifting investment decisions away from dividends and towards trading gains. In view of the above discussion, this study intends to assess the contents of dividend policies of listed companies on whether the policies enunciated by the companies are based on the parameters laid down in the regulation and provide a critical review of the assessment of the dividend distribution policy by the companies as mandated by Regulation 43A over a period of five years ever since the introduction of this requirement. By filling the research gaps in the study of dividend policy in India, scholars can provide valuable insights for policymakers, corporate managers, investors and other stakeholders. Such research can help optimise dividend policy decisions, improve corporate governance practices and enhance investor confidence in India’s financial markets.

Objectives

The objectives of the study are to examine (a) whether the dividend policies enunciated by listed companies are as comprehensive as required by the regulator, (b) whether the dividend declared was in accordance with the policy and (c) whether the policy comprised all the parameters prescribed by the regulators.

Literature Review

As research in corporate finance continues to evolve, there may be further exploration into the nuances of dividend policy in different organisational contexts. In the Indian context, a few studies have analysed the dividend behaviour of corporate firms. However, previous studies suggest that there is a rapidly growing body of research on dividend policy, with most studies concentrated in the USA and UK. Despite this, many questions regarding dividend decision-making remain unanswered, particularly in emerging markets (Pinto et al., 2020). Aivazian et al. (2003a) posited that the organisation of capital markets plays a crucial role in determining dividend policy, as companies operating in countries with well-developed capital markets are more likely to pay dividends and have higher dividend payout ratios. This observation is supported by Ferris et al. (2009), who found that firms in countries with strong shareholder protection and well-developed capital markets tend to have higher dividend payout ratios. Taxation also plays a significant role in determining dividend policy, as Ferris et al. (2009) found that firms in countries with high levels of personal taxation tend to have lower dividend payout ratios. Conversely, firms in emerging economies have been found to have a lower propensity to pay dividends and a lower payout ratio (Aivazian et al., 2003b). Glen et al. (1995) argued that this is likely due to the higher level of risk and uncertainty associated with emerging markets. Another aspect related to dividend is the determinants of dividend policy. In this regard, Kumar and Sujit (2018) conducted an empirical study of Indian firms and found that firm size, profitability and growth opportunities are important factors. Baker and Weigand (2015) identified several other factors that influence dividend decisions, including financial performance, growth opportunities, capital structure and ownership structure. Explicitly, they found that firms with higher levels of debt and those with a larger proportion of outside ownership tend to have lower dividend payout ratios. This is also supported by Guo and Ni (2008), who found that the level of institutional ownership is related to dividend policy, with firms with a higher proportion of institutional ownership tending to have a higher dividend payout ratio. There are other factors affecting dividend decisions such as the role and involvement of the board of members, especially the independent directors, in taking dividend decisions that cannot be overlooked. Gugler (2003) found that firms with a higher proportion of outside directors on their board tend to have a higher dividend payout ratio, while Gugler and Yurtoglu (2003) found that the presence of a corporate governance code is associated with a higher dividend payout ratio in German firms. Boshnak (2021) examined the impact of board composition and ownership structure on dividend payout policy in Saudi Arabian firms and found that firms with a higher proportion of independent directors and those with a higher level of family ownership tend to have a higher dividend payout ratio. Reviewing the past seminal research work relating to dividend decision provides insights into the investigation of all aspects of the subject matter as a whole and other matters allied thereof. However, while reviewing the past literature, we could not find any article on the current state of dividend policies adopted by the top Indian firms. This motivated us to investigate to what extent the companies are following the best practices in terms of their dividend policy.

Research Design

The research approach employed is prefaced on specific paradigms of unobtrusive research methods, including conceptual and document analysis. Unobtrusive research refers to methods of gathering data which do not intervene with the subjects under study (because these methods are not obtrusive). It is a kind of qualitative content analysis commonly used for analysing qualitative data. There is an ongoing demand for effective and straightforward strategies for evaluating content analysis studies (Rani & Salanke, 2023). In the context of this study, unobtrusive research was necessary to collect data without interacting with the subjects (Maroveski, 2016). Data analysis is done through an in-depth analysis of the dividend policy documents of listed firms.

For the purpose of this study, the top 200 companies by market capitalisation as on 31 March, 2021 (NSE) are selected, which covers 40% of the top 500 companies in terms of number and 88.77% in terms of market capitalisation as on the said date. The scope of the study covers whether these companies have developed their dividend distribution policies covering the individual parameters as stipulated by the said Regulation 43A and whether there is any relationship between dividend behaviour and dividend policy. The information relating to dividend distribution policy, dividend paid, dividend payout ratio, stock splits, bonus issues and listing dates in the case of new entrants during the period 8 July 2016 to 31 March 2021 (referred to hereinafter as the ‘review period’) into the top 200 companies as per NSE Market Capitalisation was taken from the following sources: (a) website of National Stock Exchange (NSE), (b) website of respective companies to the extent information is available and (c) website of Money Control. To conduct a content analysis, the authors used a three-step methodology to collect the dividend policy documents and thus evaluate their content. First, we revisited the regulatory framework in India for the dividend policy and the provisions laid down by the regulators. The necessary information pertaining to the divided distribution policy as per the provisions of the legislation was retrieved from the policy documents and categorised further for the analysis. Finally, this file was used as the primary data for the content analysis. The results of the content analysis are discussed in the next section.

Results and Discussion

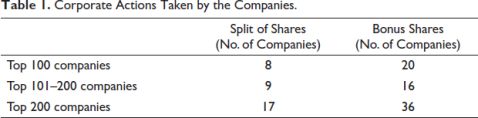

Before the analysis, the descriptions of the statistics of the select companies in terms of the number of companies listed during the review period, corporate actions such as the split of shares and bonus issuance by the companies and non-payment of dividend in terms of banking and other than non-banking sectors are mentioned below. During the review period, 25 companies got listed and entered the top 200 companies by market capitalisation. These companies were required to comply with the provisions of Regulation 43A from the date of their respective listing. During the review period, some of the companies carried out corporate actions in the form of stock splits and bonus issues, which must have impacted the amount of dividend per share. Approximately 9% of companies have undergone sub-division of shares, leading to changes in the equity structure due to the increase in the number of outstanding shares. It is important to note that stock splitting does not affect the value of existing shares. Despite an increase in the number of shares, the underlying value of each share remains unchanged. In addition to cash dividends, companies have also undertaken the corporate action of issuing bonus shares. The Companies Act 2013 and the Companies (Share Capital and Debentures) Rules 2014 outline the provisions for the issuance of bonus shares through section 63 and rule 14, respectively. The Act imposes certain conditions for the issuance of bonus shares, including that they may be issued out of free reserves, securities premium account or the capital redemption reserve account, but cannot be issued as a substitute for dividends. The details of the number of stock splits and bonus issues are provided in Table 1.

There are several reasons for firms to pay dividends such as to signal firms’ earnings quality, to return profits that are not required for investment outlays to shareholders. The companies can indicate their current situation and prospects to outside investors in the form of dividend payment and, thus, reduce information asymmetry between insiders and outsiders (Aharony & Swary, 1980; Asquith & Mullins, 1983). Therefore, it is always beneficial for a company to declare dividends. There are quite a few companies where dividends were not distributed. Non-payment of dividend appears to signal poor financial performance or inadequacy of profits. This analysis implies that dividend omissions have information content in that these firms expect lower earnings for the future. Most companies, that is, 90%, have a good track record of payment of dividends. The details of companies that skipped dividend payment in all years of the review period are provided in Table 2.

While looking further into details, we found around one-fifth of companies default in one or more than one year for the payment of dividend, signalling poor financial performance or inadequate funds. In this regard, banking companies attributed the reason(s) for skipping dividend to the RBI (Reserve Bank of India).

Compliance with the Legal Provisions

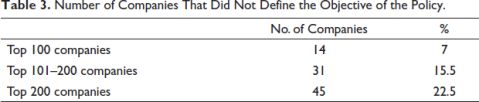

It is the responsibility of the companies to implement the dividend policy keeping in view the provisions of SEBI’s LODR Regulations and the Companies Act 2013. The purpose of the policy is to lay down in broad terms the external and internal factors including financial parameters that will be considered while deciding on the distribution of dividend, the circumstances under which shareholders of the company, may or may not expect dividend and the policy relating to retention and utilisation of earnings. Defining the objectives of the policy is an important aspect while formulating it quantifies its purpose. However, it is observed that quite a lot of companies (almost 22.5% of the companies selected) have not stated the reasons for not mentioning the objectives while formulating the dividend distribution policy. It may imply that these firms formed their policy just to comply with the regal requirements (Table 3).

As regards the companies that have specified the objects of adoption of dividend distribution policy, a perusal of the objective as stated by the companies reveals that, by and large, the following are the objects that have been adopted in the policy:

We found only four companies, including three in the top 100, have mentioned that the objective of the Dividend Distribution Policy follows Regulation 43A of the LODR. The Regulation also mandates that the dividend distribution policy needs to specify the circumstances under which the shareholders of the listed entities may or may not expect a dividend. The research studies argue that there could be various circumstances affecting dividend decisions (Jensen & Meckling, 1976; Rozeff, 1982). For example, the firms choose to finance their positive NPV (net present value) project outlays through cheaper internally generated retained earnings instead of raising costly external finance from the capital markets (Myers & Majluf, 1984). Therefore, the firms facing higher investment opportunities and, thereby, higher fund requirements will pay lower dividends to investors to reduce dependence on costly external finance raised from the capital markets (Myers, 1984). The policy statement on the circumstances under which the shareholders may or may not expect benefit investors to take a buy, hold or sell decision especially based on the first three quarters’ performance. However, one of the striking aspects that have been noticed is that almost 34% have not addressed this requirement of the policy. Surprisingly, around one-third of the sample companies identified above can be considered in terms of inadequacy of transparency with respect to dividend policy. Some of the circumstances/justifications for not adhering to the dividend payment, declared by the 65% companies, are as follows:

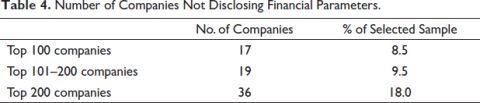

Another important aspect of dividend decisions is the consideration of financial parameters as they involves the outflow of cash. In this regard, the Regulation clearly requires the dividend distribution policy to include the financial parameters based on which dividend will be paid. It is noticed that out of the sample selected for study, 18% have not clearly disclosed the financial parameters based on which dividend will be declared/paid, as detailed in Table 4.

From an analysis of the various financial parameters stated by those companies that have disclosed these parameters, it is noticed that the following financial parameters are given weightage for the determination of the amount of the dividend to be paid:

Requirement to transfer to debenture redemption reserve, capital redemption reserve and any other statutory reserve which reduces the availability of profits available to the equity shareholders

Dividend payout ratios of comparable companies

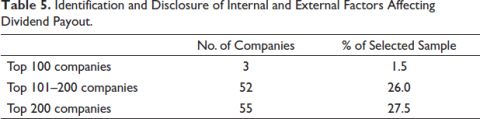

There is ample research work on internal and external factors affecting the dividend decisions (Pinto et al., 2020). For example, Mueller (1972) argues that every company has a well-defined life cycle, and the firm’s dividend payment decision varies across its different life-cycle stages. Mature firms have fewer investment opportunities, more accumulated earnings and less systematic risk and, thus, pay more dividends to investors (Denis & Osobov, 2008). The distribution of dividends is also affected by the level of free cash flow. In fact, it reduces the excess of free cash flow in the hands of managers, thereby reducing the agency problem (Jensen & Meckling, 1976). External factors such as changes in the macro-economic environment also affect the dividend decision (Pandey, 2022). The Regulations require the dividend distribution policy to identify the internal and external factors to be considered for declaration of dividend separately. From an understanding of Regulation 43A of LODR as prescribed by SEBI, it appears that since the financial parameters are separately prescribed, the internal and external factors that influence the dividend recommendation and declaration should be other than financial parameters. However, it is noticed that in the case of 55 companies, though the financial parameters and internal and external factors have been covered, they have been merged under the same head. The details are given in Table 5.

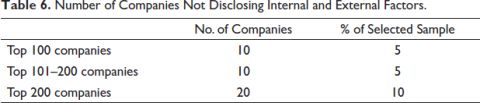

As regards the inclusion of the internal and external factors that must be considered for declaration of dividends in the dividend distribution policy, it has been noticed that in the case of 20 companies, these have not been specifically disclosed (Table 6).

The companies that have addressed this requirement have inter alia disclosed the following internal and external factors:

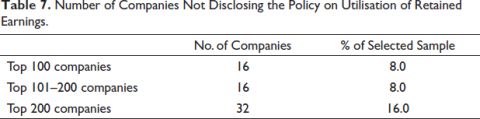

Another important requirement is with respect to stating in the dividend distribution policy how the retained earnings will be utilised. There are various aspects pertaining to the retained earnings. For instance, Higgins (1972) finds evidence that larger firms are less dependent on internal funds as they have an advantage in raising external funds from the capital markets. Therefore, retention of profit would be less. We found that 32 companies do not mention in the policy about utilisation of retained earnings (Table 7).

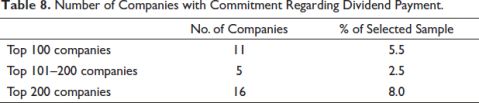

In the case of companies that disclosed the policy with respect to utilisation of retained earnings, it is observed that that companies disclosing their policies regarding the utilization of retained earnings prioritize various strategies aimed at fostering growth, financial health, and shareholder value. The common purposes outlined for utilizing retained earnings include developing new products, conducting research and development, or investing in subsidiaries, joint ventures (JVs), or associates. Some companies also cited the reasons for the buy-back of shares for ploughing back of profit, while a few companies retained their earnings for meeting requirements of long-term working capital and repayment of debts. It is noticed that some companies have given clear commitment/indication regarding dividend payment as part of the dividend distribution policy, subject of course to applicable statutory provisions. The details are given in Table 8.

The commitment/indication given regarding dividend by these companies are along the following lines:

In the case of two banks, not exceeding 40% of profits after tax is subject to RBI guidelines

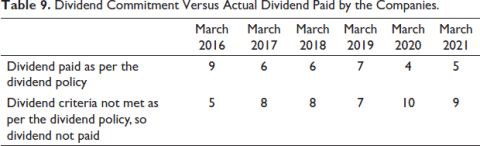

It is quite admissible that a company may not fulfil its commitment towards dividend payment. There are merely 16 companies that mentioned their dividend commitment in dividend policy. We studied 14 companies’ dividend payout behaviour post the dividend policy. As per Table 9, all sample companies adhere to their commitment.

Companies with Deficiencies in the Dividend Policy

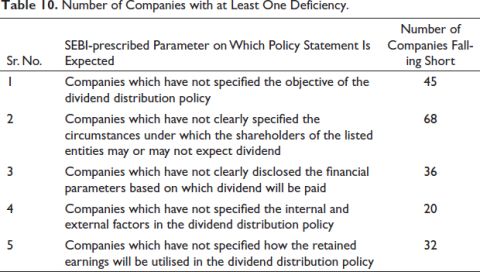

SEBI has prescribed five broad parameters on which the dividend policy is expected to have made policy statement/disclosure. However, based on the above analysis, an observation is made in our sample data that companies are identified with at least one or two deficiencies in making policy statements on various parameters prescribed by SEBI in their policy. A summary of observations is given in Table 10.

It is very interesting to note that one-third of companies are falling short on account of not clearly specifying circumstances under which the shareholders of the listed entities may or may not expect a dividend. Twenty per cent of the companies have not specified the objectives of the policy. Moreover, nearly one-fifth of the companies did not disclose the financial parameters based on which dividend will be paid (Table 11).

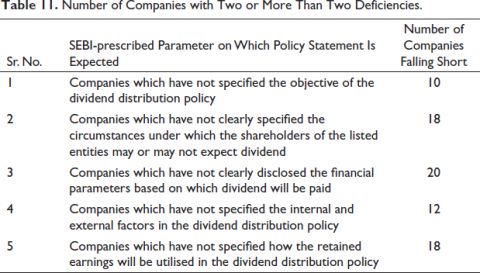

There are quite a few identified companies with more than one discrepancy while framing their policies. There are 34 companies with two or more deficiencies in incorporating policy statements on prescribed parameters. No company was found deficient in all five parameters except Nestle, with four deficiencies. Nestle Ltd. prepared a policy statement on the objective of the policy but was found wanting on the other four parameters. Thirty-eight companies did not make a policy statement on how retained earnings will be used. In view of the above results and discussion, it is notable that there is a large proportion of the companies disregarding the parameters required by the regulators. The purpose of disclosing the dividend policy is to provide clarity to shareholders regarding the distribution of dividends and to aim at promoting transparency. However, by and large it appears that the dividend payouts are guided by a consideration of the board’s long-term strategy. In fact, looking from the investors’ perspective, having in place a dividend distribution policy on the part of companies has probably not addressed their needs.

Conclusion and Future Implications

The topic of dividends continues to generate significant discussion and merits thorough examination. The dividend policy is intended to reward shareholders by allocating a portion of profits for distribution, while retaining sufficient funds for future business needs and growth prospects, considering external factors such as the national economy and the financial strength of the company and its material subsidiaries. Based on the perusal of the dividend distribution policy documents of selected top 200 companies and the dividends declared by them, after considering the earnings available for equity shareholders, stock splits, bonus issues and requirement of internal accruals for company’s operations, by and large it appears that the dividend payouts are guided by a consideration of the board’s long-term strategy. From an investor perspective, however, having in place a dividend distribution policy on the part of companies has probably not addressed their needs of what returns can be clearly expected from an investment in these companies. In fact, most companies have not clearly indicated what dividend can be expected by the investors. Perhaps, SEBI may consider mandating a greater clarity in the dividend distribution policy. However, the bigger questions that remain from a regulatory perspective are: Are the dividends declared in conformity with the adopted policies? Has there been a departure from the policy and whether such departures are disclosed in the directors’ report? These questions relating to compliance and governance can be better addressed by providing a framework for independent review on an annual basis. Perhaps the way forward is to stipulate a requirement for the companies to disclose either in the directors’ report or in the corporate governance report about any departure from the dividend distribution policy and the reasons for the same. Further, the regulations may provide for a minimum commitment on dividend, subject to compliance of identified statutory requirements and review of the compliance of the dividend distribution policy by an independent professional.

Acknowledgement

The authors are grateful to the anonymous referees of the journal for their extremely useful suggestions to improve the quality of the article. Usual disclaimers apply.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

ORCID iD

Shweta Mehrotra Https://orcid.org/0000-0002-7229-199X

Aharony, J., & Swary, I. (1980). Quarterly dividend and earnings announcements and stockholders’ return: An empirical analysis. The Journal of Finance, 35(1), 1–12.

Aivazian, V., Booth, L., & Cleary, S. (2003a). Dividend policy and the organization of capital markets. Journal of Multinational Financial Management, 13(2), 101–121.

Aivazian, V., Booth, L., & Cleary, S. (2003b). Do emerging market firms follow different dividend policies from US firms? Journal of Financial Research, 26(3), 371–387.

Al-Najjar, B., & Kilincarslan, E. (2017). Corporate dividend decisions and dividend smoothing: New evidence from an empirical study of Turkish firms. International Journal of Managerial Finance, 13(3), 1–38. https://doi.org.10.1108/IJMF-10-2016-0191

Asquith, P., & Mullins, D. W. (1983). The impact of initiating dividend payments on shareholders’ wealth. Journal of Business, 56(1), 77–96.

Baker, H. K., & Weigand, R. (2015). Corporate dividend policy revisited. Managerial Finance, 41(2), 126–144.

Balasubramanian, B. N., & Anand, R. (2013). Ownership trends in corporate India 2001–2011: Evidence and implications (IIM Bangalore Research Paper No. 419). http://doi.org.10.2139/ssrn.2303684

Black, F. (1976). The dividend puzzles. The Journal of Portfolio Management, 2(2), 5–8.

Black, F., & Scholes, M. (1974). The effects of dividend policy on common stock prices and returns. Journal of Financial Economics, 2, 1–22.

Boshnak, H. A. (2021). The impact of board composition and ownership structure on dividend payout policy: Evidence from Saudi Arabia. International Journal of Emerging Markets. https://doi.org.10.1108/IJOEM-05-2021-0791

Burkart, M., Gromb, D., & Panunzi, F., (1997). Large shareholders, monitoring, and the value of the firm. The Quarterly Journal of Economics, 112(3), 693–728.

Chakrabarti, R., Megginson, W., & Yadav, P. K. (2008) Corporate governance in India. Journal of Applied Corporate Finance, 20, 59–72.

Claessens, S., Fan, J. P., & Lang, L. H. (2006). The benefits and costs of group affiliation: Evidence from East Asia. Emerging Markets Review, 7(1), 1–26.

Fama Eugene, F. (1974). The empirical relationships between the dividend and investment decisions of firms. The American Economic Review, 64(3), 304–318.

Ferris, S. P., Sen, N., & Unlu, E. (2009). An international analysis of dividend payment behavior. Journal of Business Finance and Accounting, 36(3–4), 496–522.

Glen, J. D., Karmokolias, Y., Miller, R. R., & Shah, S. (1995). Dividend policy and behavior in emerging markets: To pay or not to pay. In IFC Discussion Paper. The World Bank. http://agris.fao.org.agris-search/search.do?recordID=US2012421063

Gugler, K. (2003). Corporate governance, dividend payout policy, and the interrelation between dividends, R&D, and capital investment. Journal of Banking and Finance, 27(7), 1297–1321. https://doi.org.10.1016/S0378-4266(02)00258-3

Gugler, K., & Yurtoglu, B. B. (2003). Corporate governance and dividend pay-out policy in Germany. European Economic Review, 47(4), 731–758. https://www.sciencedirect.com/science/article/pii/S001429210200291X

Guo, W., & Ni, J. (2008). Institutional ownership and firm’s dividend policy. Corporate Ownership and Control, 5(2), 128–136.

Higgins, R. C. (1972). The corporate dividend-saving decision. Journal of Financial and Quantitative Analysis, 7(2), 1527–1541.

Jensen, M. C., & Meckling, W. H. (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3(4), 305–360.

Kumar, B. R., & Sujit, K. S. (2018). Determinants of dividends among Indian firms: An empirical study. Cogent Economics and Finance, 6(1), 1423895. https://doi.org.10.1080/23322039.2018.1423895

Lintner, J. (1956). Distribution of incomes of corporations among dividends, retained earnings, and taxes. The American Economic Review, 46(2), 97–113.

Maroveski, R. (2016). Techniques in secondary data collections: A beginners’ guide. Trafford.

Modigliani, F., & Miller, M. H. (1958). The cost of capital, corporation finance, and the theory of investment. The American Economic Review, 48(3), 261–297.

Mueller, D. C. (1972). A life cycle theory of the firm. The Journal of Industrial Economics, 20(3), 199–219.

Myers, S. C. (1984). The capital structure puzzle. The Journal of Finance, 39(3), 574–592.

Myers, S. C., & Majluf, N. S. (1984). Corporate financing and investment decisions when firms have information that investors do not have. Journal of Financial Economics, 13(2), 187–221.

Pandey, S. (2022). An empirical study of the movement of sectoral indices and macroeconomic variables in the Indian stock market. IMIB Journal of Innovation and Management, 1(2), 82–93

Pinto, G., Rastogi, S., Kadam, S., & Sharma, A. (2020). Bibliometric study on dividend policy. Qualitative Research in Financial Markets, 12(1), 72–95. https://doi.org.10.1108/QRFM-11-2018-0118

Rani, A., & Salanke, P. (2023). A bibliometric analysis on business and management research during COVID-19 pandemic: Trends and prospects. IMIB Journal of Innovation and Management. https://doi.org.10.1177/ijim.221148834

Rozeff, M. S. (1982). Growth, beta and agency costs as determinants of dividend payout ratios. Journal of Financial Research, 5(3), 249–259