IMIB Journal of Innovation and Management

Search

Search

Anshu Duhoon1 and Mohinder Singh1

and Mohinder Singh1

1Department of HPKV Business School, School of Commerce & Management Studies, Central University of Himachal Pradesh, Himachal Pradesh, India.

Creative Commons Non Commercial CC BY-NC: This article is distributed under the terms of the Creative Commons Attribution-NonCommercial 4.0 License (http://www.creativecommons.org/licenses/by-nc/4.0/) which permits non-Commercial use, reproduction and distribution of the work without further permission provided the original work is attributed.

Like other business forms, corporate governance is a matter of concern for family firms as well. The objective of the work is to study the corporate governance practices of family-owned firms using bibliometric analysis of existing literature. With the help of VOSviewer & Biblioshiny Software, an attempt has been made to develop the visualization patterns based on academic publications growth, most influential authors, country, keyword occurrences, thematic map and co-authorship network. Based on 435 studies conducted during the selected period, the study found the maximum work has been done in the USA followed by Italy, Spain, China and UK, and Anderson and Reeb (2003) is the most cited work in this area. The main focus of prominent studies was on assessing the impact of family ownership on a firm’s performance, and there is unanimity that family firms’ CEOs devote more time and effort to preserve socio-economic wealth, have fewer forecasting errors and perform better. Though ‘corporate strategy’ and ‘governance approach’ are key concepts in family businesses yet it is a less explored areas. Thiss article provides an overview of how the literature on corporate governance and family firms has evolved and a synopsis of the most influential authors, most productive countries, co-word analysis and themes clustering. This study provides a thorough coverage of the existing literature on family governance mechanisms and is helpful for new researchers who want to understand this concept and also for those who are looking to explore new directions in the same field.

Corporate governance, family firms, bibliometric analysis, Scopus

Introduction

Corporate governance aims to ensure fairness and transparency in all managerial decisions for the protection of the interest of investors and other related stakeholders. According to OECD (2019), corporate governance ensures that the interests of all the stakeholders within and outside the business are taken care of. With time, it has gained equal relevance to family-run businesses as well. Corporate governance is concerned with ownership structure, principal–agent conflicts, board composition and strengthening the firm’s performance (Ehikioya, 2009). The ownership structure is one of the key elements of corporate governance as it determines who has the authority to make decisions for the company (Zattoni, 2011). Family-owned firms are more complex than publicly listed companies, due to the need of preserving the harmony between the interest of the family and the company (Howorth & Kemp, 2019; Kabbah de Castro et al., 2017). The introduction of corporate governance in family businesses aims to resolve conflicts between majorities (family members) and minorities shareholders and to build transparency to promote stakeholders’ interest (Kaur & Singh, 2018), through effective board monitoring, quality audit and disclosure transparency (Sarbah & Xiao, 2015). In family businesses, the effectiveness and competency of the group can be a great asset for the economy, but if these groups act unethically, they can become liabilities for the economy. The management and expansion of family enterprises are affected by corporate governance components. Corporate governance mechanisms significantly contribute to taking effective and quality decisions (Shivani et al., 2017). But if corporate governance mechanisms are weak in the family group, it can decrease the efficiency of the firm (Morck & Yeung, 2003).

The interrelationship between family ownership and corporate governance is an emerging area of discussion among academicians and researchers (Chen et al., 2008; Hasan et al., 2014; Jiang & Peng, 2011; Kowalewski et al., 2010; Mohd & Wi, 2003; Peng & Jiang, 2010). Most of the prominent authors (Anderson & Reeb, 2003; Andres, 2008; McConaughy & Walker, 1998) have shown that family firms are performing well and also have better long-term investment vision (James, 1999) in comparison to non-family firms. Chua et al. (1999) have defined a family firm as an organisation that is governed or controlled by the ‘same family or a small number of families in a manner that is potentially sustainable across a generation of the family or families’. According to the report published by the Boston Consulting Group in 2017, approximately 60% to 85% of enterprises globally are regulated or controlled by families (Bhalla & Orglmeister, 2017). Family firms are playing a significant role in ‘wealth creation, wealth preservation and wealth distribution’ in the nations (Priya, 2021). The governance structure of the family firms is different from that of non-family members (Daily & Dollinger, 1992) because of differences in goals and ownership structure (Bettinelli, 2011).

In addition to focusing on long-term sustainability (Mandl, 2008), family ownership also improves company performance by cutting agency costs (Minh Ha et al., 2022). Simultaneously, some studies (Mani & Lakhal, 2015; Pearson et al., 2008; Salvato & Melin, 2008) suggest that family-owned boards have high productivity, are more efficient (McConaughy & Walker, 1998) and create high firm value (Eugster & Isakov, 2019; Koji et al., 2020). In contrast to these findings, many researchers (Claessens et al., 2000; DeAngelo & DeAngelo, 2000; Villalonga & Amit, 2006) have also talked about how the large number of family members on the board might exploit minorities for personal benefits. The presence of more family members can lead to another type of conflict, known as Agency Problem II (The exploitation of the minority shareholders by controlling shareholders, a different sort of conflict from Agency Problem I as explained by Ballantine et al. (1932) and Jensen (1986). Cucculelli and Micucci (2008) and Miller et al. (2007) analyse the behaviour of family businesses and find that when family members hold the majority of ownership, they prioritise their interests over those of the business, which resulted in lower productivity (Barth et al., 2005).

Family businesses encompass some of the biggest corporations in the world, and their economic impact is still enormous (Peng & Jiang, 2010). Even though researchers and academics are paying attention to this topic, it still requires more development (Pieper, 2003; Rovelli et al., 2022). The available literature on the governance structure in family enterprises has yielded conflicting results, so the current study aims to comprehend, examine and identify the key themes in that literature. By using the bibliometric review methodology, this study seeks to address the following research issues:

This study contributes significantly to understand the governance mechanisms of family firms by conducting an inclusive analysis of the related literature. The other sections of article are formulated as follows. The second section briefly discusses about theoretical framework, rationale and objectives of the study. The third section explains the research methodology. The fourth section is related to analysis and interpretation of the data. The fifth section discusses the conclusion, implications and directions for future research.

Theoretical Framework

There is no universal definition of family-owned firms, different authors have explained this concept in their terms. According to Anderson and Reeb (2003), family firms should own stock in the companies and have a representative on the board. While in terms of McConaughy et al. (2001), the CEO of family businesses should be a founding member or a descendant of the founding family. In family businesses, the decision-making process is influenced by the family members present on the board (Srivastava & Bhatia, 2022). Because of majority shareholding and decision-power concentration, family firms are often criticised (Gómez-Mejía et al., 2007; Ponomareva & Ahlberg, 2016). There are many other issues such as Agency Problem II (due to the dominance of family members in decision-making), weak internal governance mechanisms and managerial opportunistic behaviour arise the question of the need for effective corporate governance mechanisms in family firms (Buachoom & Amornkitvikai, 2022; Lubatkin et al., 2005; Siebels & zu Knyphausen-Aufseß, 2012). Family firms use different forms of internal and external governance mechanisms to solve their family conflicts (Lane et al., 2006; Shleifer & Vishny, 1986) and perform better than non-family firms in the complex and competitive business environment (van Essen et al., 2015). Though, some bibliometric analysis has been done on the corporate governance practices of family-owned firms to understand the involvement of women in decision-making in family businesses (Maseda et al., 2022), trends of publication in the family firm’s domain (Araya-Castillo et al., 2022; Rovelli et al., 2022) and to observe the degree of legal protection given to minority owners (Aguilera & Crespi-Cladera, 2012) explained in their review paper that how varies by country and how this influences family businesses’ adherence to governance standards. Still, there is a lack of studies that give a thorough overview of the development of governance structures in family firms. So, this study contributes by providing a comprehensive analysis of corporate governance mechanisms in family firms.

Rationale of the Study

The corporate governance structure adopted by the organisations has a considerable impact on the performance of the family businesses (Vazquez et al., 2020) and also aids in solving family conflicts (Miller & Le Breton-Miller, 2006). Numerous studies are focusing on family firm governance but, still, it is not fully evolved and required further validation (Suess, 2014). With the increasing importance of governance in family firms, a bibliometric analysis focusing on corporate governance practices of the family-owned firm can be an important initiative to elucidate further the trend, present scenario and potential for future research on this topic. The present study is an attempt in this context.

Objectives of the Study

The main objective of the article is to study the growth, trends, pattern, main authors, core themes and unexplored areas in the studies focusing on corporate governance practices of family-owned firms.

Research Methodology

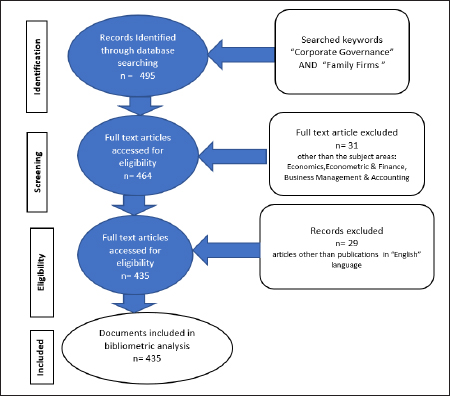

The study has followed the PRISMA (Preferred Reporting Items for Systematic Reviews and Meta-Analyses) guidelines as proposed by Moher et al. (2009) to extract the relevant studies from the Scopus database (Figure 1). In the first stage, only published research articles were extracted from the Scopus database using ‘corporate governance’ and ‘Family Firm’ as the keywords, and 495 research articles were identified at this stage. In the second stage, articles published in the subject domains, that is, Business Management, Accounting, Finance, Economics and Econometric Finance were retained, which limits the number to 464. Thereafter 29 research papers published in other than the English language were also excluded and finally 435 research articles were considered for further research.

The study applied the bibliometric technique to summarise and categorised the bibliographic data (Debicki et al., 2009; Ferreira et al., 2019) and to explore the quantitative changes and publication propensity in the studies conducted on the theme ‘corporate governance in family firms’ (De Bakker et al., 2005; Merigó et al., 2015).

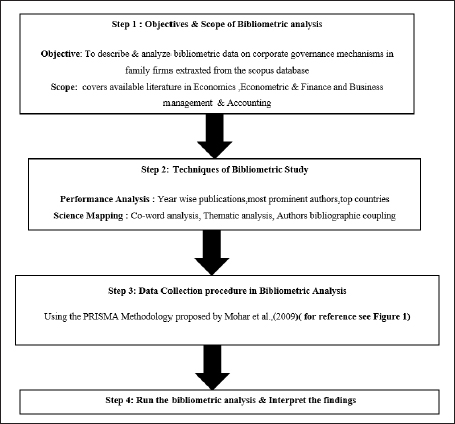

The bibliometric technique evaluates the existing literature in a certain field to determine current research trends based on themes, citations, publication growth and other relevant research components (Ali et al., 2020; Paul & Criado, 2020; Wallin, 2005). Pritchard (1969) in his study defined the bibliometric method as a ‘new discipline where quantitative methods were employed to probe scientific communication process by measuring and analysing various aspects of written documents’. The adoption of the bibliometric review method is very significant to have an inclusive understanding of the scientific literature related to that field (Durieux & Gevenois, 2010). A summarised view of the criteria used for the selection of the relevant literature for doing bibliometric analysis is exhibited in Figure 2.

Figure 1. PRISMA Flow Diagram.

Figure 2. Bibliometric Method Steps.

Data Analysis and Interpretation

To answer all formulated research questions, the performance mapping technique has been used. Performance mapping technique is a method of bibliometric review analysis, that is descriptive and focuses to examine and to present the performance of selected research constituents related to a particular field (Donthu et al., 2021a; Mas-Tur et al., 2021). The first three questions have been addressed with help of the performance analysis technique. To answer the last question authors have applied the science mapping method. Science mapping displays the structural interconnection and interaction among the different aspects of a research field (Donthu et al., 2021b). For creating the visualisation network two software, that is, VOSviewer software and the Biblioshiny package of Rstudio software have been used. Thematic networking diagram is constructed by using the Biblioshiny package, and keyword analysis & authors’ bibliographic coupling maps are created through VOSviewer.

Growth of Literature

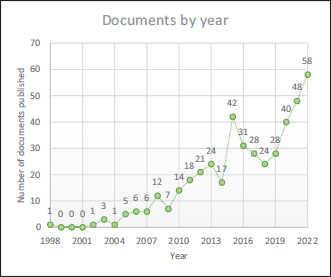

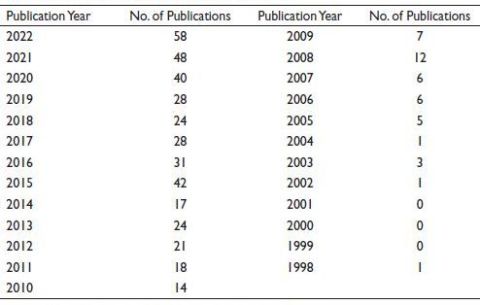

It is seen from the publication trend (Figure 3 and Table 1) that the first publication related to the field was recorded in the Scopus database in 1998. However, continuity in publications was noticed from 2007. There was a stable growth in publications from 2002 to 2007, but then significant growth was noticed in 2008 (12 documents) and then in 2015 (42 documents). The maximum number of publications was recorded in 2022 (58 documents, 13.33%). This upward trend is showing increasing concern among researchers and academicians in this research area.

Figure 3. Number of Documents Published per Year.

Table 1. Year-Wise Publications from 1998 to 2022.

Source: Annual distribution of the literature in Scopus database.

Most Prominent Authors

Table 2 highlights the top 10 most cited authors with the title of publications and their total citations, and it has been observed that Anderson R.C. with 829 citations is the most cited author followed by Burkart M. with 737 citations and both having single publications. Thus, these two publications are most significant to understand the corporate governance behaviour of family-owned enterprises. The study titled ‘Founding family ownership and the agency cost of debt’ by Anderson and Reeb (2003) is the most cited article, which discussed about the impact of family ownership on firm’s performance. The study concluded that the family firms’ performance is much better than non-family firms due to the presence of family CEO on board. Although Kellerman has the highest number of publications (n = 6) with 390 citations, but their citations are comparatively very less in numbers than the authors with a few publications, such as Anderson R.C. (n = 1) with 829 citations, Burkart M. (n = 1) with 737 citations, Ali A. (n = 1) with 585 citations, Jiang Y. (n = 3) with 490 citations and Carney M. (n = 4) with 427 citations. In the next paragraph, highly cited publication of top 10 prominent authors have been explained (Table 2).

Out of his six publications, Kellerman (Gedajlovic et al., 2012) received the most citations (307 citations) for his review work titled ‘The Adolescence of Family Business Research: Taking Stock and Preparing for the Future’ and concluded that family firms devote more time and effort to preserve the socioeconomic wealth of the firm as compared to non-family firms. The second most cited work in this area is Burkart et al. (2003). In this study, the authors explained the repercussions of the agency’s two problems, that is, (between majority and minority shareholders), and argued that the legal protections offered to minority shareholders play a significant role in deciding the role of family members in the firm’s management. (Ali et al., 2007) in their study titled ‘Corporate Disclosure by Family Firms’ analysed the disclosure practices of family firms and found that the family firms have fewer forecasting errors, bid-ask spreads and lower analysts’ dispersion as compared to the non-family firms. The fourth most cited work with 304 citations, that is, ‘Institutions behind family ownership and control in large firms’, by Peng and Jiang (2010) concluded that the corporate governance mechanisms—ownership, CEO position, pyramid structure and institutional development—have a significant impact on firm’s value. The study conducted by Fernández and Nieto (2006) have 400 citations worked on understanding the role of the family in scaling the firm to the international level and observed that family ownership has a negative effect on internalisation. The firm having corporate ownership has scaled to the international level. The study titled ‘Family Firm Governance, Strategic Conformity and Performance: Institutional vs. Strategic Perspectives’ by Miller D. & Le Breton-Miller (authors ranked 8th and 10th in most cited authors) argued that strategic conformity is more prevalent in businesses where family members serve as CEO. But this strategic conformity is found to be associated only with high return on assets not with firm value. While analysing the impact of family manager’s characteristics on firm’s performance, Minicilli A., tested the moderation effect of family dominance and noticed that non-family team diversity plays a significant role in firm performance and the family dominance (i.e., proportion of family members on board), have a positive moderating effect.

.jpg)

Country-Wise Scientific Production

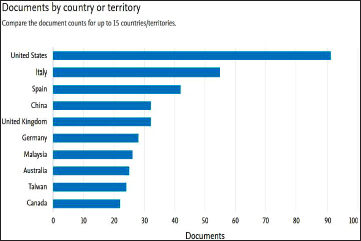

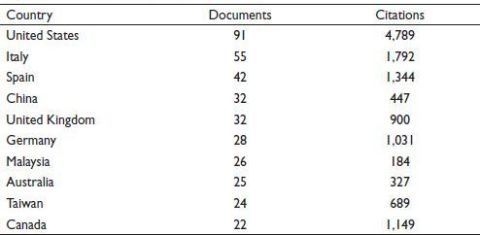

Figure 4 presents the top 10 countries where studies on corporate governance practices of family-based firms have been conducted. It may be observed from the study that the majority of the research works have been concentrated within the realm of highly developed countries such as the United States (N = 91), Italy (N = 55), Spain (N = 42), United Kingdom (N = 32), Germany (N = 28), Australia (N = 25) and Taiwan (N = 24). Only 3 developing countries make it into the top 10, and those are China (N = 32), Malaysia (N = 26) and Canada (N = 22). In terms of citations, Table 3, the studies conducted in the USA have the highest number of citations (4,789) followed by Italy (1,792), Spain (1,344) and Canada (1,149). China and the U.K. have only 32 publications but not enough to make a significant impact in terms of citations compared to the publications of Germany and Canada.

Figure 4. Top 10 Countries Having Maximum Number of Publications.

Source: Extracted from the Scopus database.

Table 3. Top 10 Most Influential Countries.

Keywords Visualisation Network

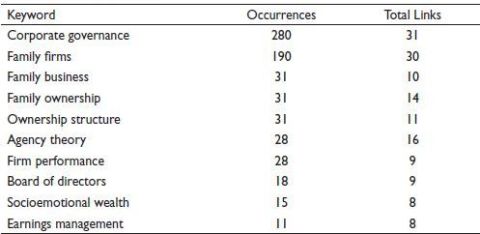

Table 4 indicates the top 10 keywords based on their frequency and total links. The size of nodes in the keyword visualisation network reflects the frequency of keywords; the larger the size, the higher the frequency of keywords (Viana-Lora & Nel-lo-Andreu, 2022). The keyword clusters are formed based on co-occurrence network and each keyword has different density (Dharmani et al., 2021). The corporate governance node has the highest occurrences (280), followed by family firms (190), family business (31), family ownership (31), ownership structure (31), agency theory (28), firm performance (28), board of directors (18), socioemotional wealth (15) and earning management (11).

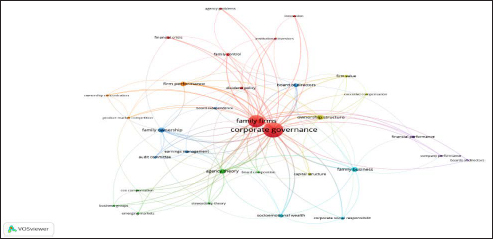

Authors’ keywords are grouped into five clusters (Figure 5). The red cluster shows smallest distance between the node ‘family firm’ and ‘corporate governance’, which means that these two keywords have a strong relationship compared to other items that fall in the same cluster, that is, agency problem, dividend policy, family control, financial crisis, institutional investors and innovation. Orange cluster is centred by firm performance and shows the correlations with other nodes such as ownership concentration, product market competition and corporate governance. The green cluster indicates the interlink among the agency theory, board composition, business group, CEO compensation, market perception and stewardship theory. The concept of family ownership (blue cluster) has been explored by the researchers in the context of audit committees, board independence, board of director’s composition and earning management. The yellow cluster explains the inter link between firm value, dividend structure, executive compensation and ownership structure. The thickness of the link shows the co-occurrence of the keywords resembling similar research work and also an overview of the areas that are interlinked but still unexplored (Donthu et al., 2021a).

Table 4. Top 10 Keywords.

Figure 5. Keywords Cluster Map.

Source: Co-word analysis in VOSviewer software.

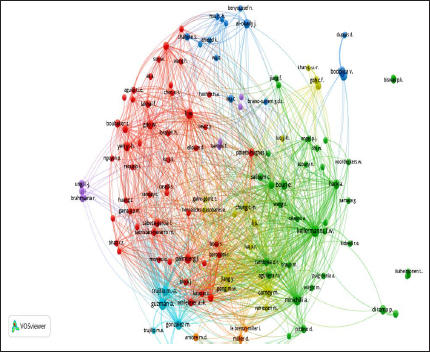

Bibliographic Coupling of Authors

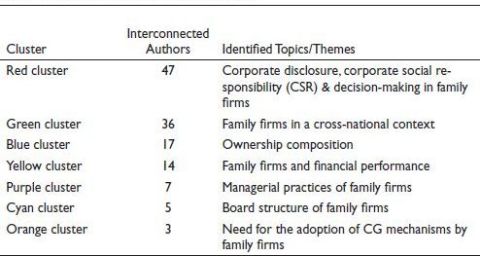

Bibliographic coupling is a science mapping technique based on the assumption that publications with shared references also have similarities in the contents (Weinberg, 1974). Donthu et al. (2021a) and Zupic and Čater (2015) emphasised the importance of bibliographic coupling and stated that in this analysis, publications are grouped into themes due to shared references. Figure 6 visualises the bibliographic network of the authors. All authors have been classified into seven clusters based on the intellectual linkage in their work (Table 5). Cluster 1 (Red cluster) is anchored by 47 authors working on the heterogeneous themes ‘corporate governance’, ‘corporate social responsibility’ (CSR) and ‘decision making’ in family firms. The second cluster (green) indicates the tendency of authors towards the performance of family firms in ‘cross-national’ context. The third cluster (blue) consists of authors who tend to analyse the ‘ownership composition’ in family firms. The generalised theme in the yellow cluster refers to the impact of family ownership on the ‘financial performance’ of the firms. The purple cluster consists of authors who have focussed on studying the ‘managerial practices’ in family firms. Cyan cluster consists of authors who have explored the impact of ‘board structure’ on family firm value, and the orange cluster consists of authors who have explained the ‘need for the adoption of CG practices’ in family firms. The bibliographic coupling method is based on the notion that two papers that cite a third paper are highly connected and ought to be grouped together in the visualisation map’s cluster solution.

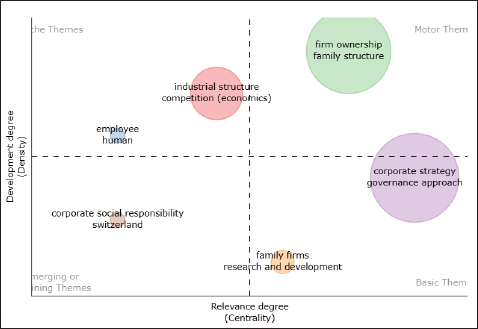

Thematic Map

The thematic map represents the centrality on the X-axis and density on the Y-axis of the keywords cluster. In the thematic mapping method, interconnections between the cluster formed based on the author’s keywords are analysed to obtain relevant themes. Centrality symbolises the degree of interaction while density is about the ‘internal strength’ of a cluster (Agbo et al., 2021). There are four quadrants in the thematic map, and each quadrant has a different theme (Sobjak

et al., 2023). The quadrant of upper right is depicted for motor themes contains ‘family structure’ and ‘firm ownership’. Motor themes are considered to be well-developed and also crucial for structuring the research field. The lower left quadrant is devoted to the emerging concept which is ‘corporate social responsibility’. But the influence of CSR on the evolution of the family firm notion is not very significant. The lower right quadrant reveals that—‘corporate strategy’ and ‘governance approach’ are the fundamental concepts in the context of family-owned enterprises but need further validation. In the upper left quadrant, niche and well-developed issues such as ‘industrial structure’ and ‘market competition’ can be seen (Figure 7).

Figure 6. Bibliography Coupling.

Source: Bibliography coupling (authors) clusters created by using VOSviewer software.

Table 5. Interconnected Co-Authors Clusters.

Figure 7. Thematic Map.

Source: Created by the authors using Biblioshiny (Rstudio software).

Conclusion and Discussion

Most of the firms worldwide are family owned in nature (Gedajlovic et al., 2012; Hiebl et al., 2018) and play a significant role in employment creation (Carsrud & Brännback, 2012). The growth of family firms also depends upon governance practices adopted by the firms. This study is focused on studying the evolution of corporate governance practices in family-owned businesses. The first publication in the Scopus database was reported in 1998 and the graph shows a tremendous growth rate. The most prominent study (Anderson & Reeb, 2003) concludes that corporate governance plays a significant role in resolving family conflicts and in developing an atmosphere of business transparency, trust and fairness within the organisation. The authors Anderson and Burkart are found as most prolific authors, and the most productive countries are found to be USA, Italy and Spain.

For finding the most prominent themes, keywords networking diagram and thematic mapping methods were used. Keywords networking analysis identifies that ‘innovation’, ‘product market competition’, ‘corporate social responsibility’, ‘financial crisis’ and ‘socio-economic wealth’ are less explored concepts int he context of family firm literature. So, these areas can be further explored to have a better understanding of family firms’ behaviour and to give new directions for future research. Thematic analysis suggests that corporate strategy and governance approach are the basic themes related to the field but are still unexplored. It also shows that industrial structure and competition are well-developed themes, but more efforts are needed to establish their link with the family businesses. The most significant authors and their collaborative efforts in the field of family governance are displayed by the bibliographic co-authorship network. This network identifies ‘corporate disclosure’, ‘corporate social responsibility’, ‘decision-making power’, ‘managerial behaviour’, ‘ownership composition’, ‘board structure’ and ‘governance mechanisms’ in family firms as the core themes in the existing studies. Family-owned firms are more engaged in CSR activities and more financial transparency due to their reputation concern. In addition to resolving disputes and fostering harmony among the family board, an effective governance framework is substantial for long-term survival in the market.

Implications

The study is an attempt to review the existing literature on significance of the corporate governance practices of family firms and may help the academicians and practitioners in better understanding the insinuation of family firm’s governance practices and its impact on its growth as well as to identify potential themes for future research work. Bibliometric review is the theoretical representation of available literature, so this study can also serve as a foundation for other literature review methods like meta-analysis and systematic review, and also for empirical studies.

Limitations and Future Research Directions

The bibliometric analysis is a useful tool for exploring and identifying research gaps in the literature but not devoid of limitations (Wallin, 2005). A somewhat more pertinent limitation emanates from the fact that research papers/studies examined have been extracted only from Scopus database. This study did not consider the articles from other databases such WoS Index, EBESCO, Google Scholar and other eminent databases, which limits the generalisation of findings. So future studies can add to this field by considering all these databases. This study is limited only on to understand the corporate governance framework in family-owned firms; hence, future research may explore other factors such as social capital, competitive advantage, financial performance and stock market behaviour in context of family firms. However, despite these shortcomings, the study will be helpful to the researchers in acknowledging the earlier work and future directions in the field of family-oriented studies.

Acknowledgements

The authors are grateful to the anonymous referees of the journal for their extremely useful suggestions to improve the quality of the article. Usual disclaimers apply.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

ORCID iD

Anshu Duhoon https://orcid.org/0000-0002-8931-7068

Agbo, F. J., Oyelere, S. S., Suhonen, J., & Tukiainen, M. (2021). Scientific production and thematic breakthroughs in smart learning environments: A bibliometric analysis. Smart Learning Environments, 8(1), 1–25. https://doi.org/10.1186/s40561-020-00145-4

Aguilera, R. V., & Crespi-Cladera, R. (2012). Firm family firms: Current debates of corporate governance in family firms. Journal of Family Business Strategy, 3(2), 66–69.

Ali, A., Chen, T. Y., & Radhakrishnan, S. (2007). Corporate disclosures by family firms. Journal of Accounting and Economics, 44(1–2), 238–286.

Ali, A., Hakak, I. A., & Amin, F. (2020). Assessing the coronavirus research output: A bibliometric analysis. Global Business Review. Advance online publication. https://doi.org/10.1177/0972150920975116

Anderson, R. C., & Reeb, D. M. (2003). American Finance Association founding-family ownership and firm performance: Evidence from the S&P 500. The Journal of Finance, 58(3), 1301–1328.

Andres, C. (2008). Large shareholders and firm performance—An empirical examination of founding-family ownership. Journal of Corporate Finance, 14(4), 431–445. https://doi.org/10.1016/j.jcorpfin.2008.05.003

Araya-Castillo, L., Hernández-Perlines, F., Millán-Toledo, C., & Ibarra Cisneros, M. A. (2022). Bibliometric analysis of studies on family firms. Economic Research-Ekonomska Istraživanja, 35(1), 4778–4800.

Ballantine, H. W., Berle, A. A., & Means, G. C. (1932). The modern corporation and private property. California Law Review, 21(1), 78–79. https://doi.org/10.2307/3475545

Barth, E., Gulbrandsen, T., & Schoø, P. (2005). Family ownership and productivity: The role of owner-management. Journal of Corporate Finance, 11(1–2), 107–127. https://doi.org/10.1016/j.jcorpfin.2004.02.001

Bettinelli, C. (2011). Boards of directors in family firms: An exploratory study of structure and group process. Family Business Review, 24(2), 151–169. https://doi.org/10.1177/0894486511402196

Bhalla, V., & Orglmeister, C. (2017, September 6). A founder’s guide to professionalizing a family business. Boston Consulting Website. https://www.bcg.com/publications/2017/family-business-people-organization-founders-guide-professionalizing-family-business.aspx

Buachoom, W. W., & Amornkitvikai, Y. (2022). The moderating effects of board independence and the separation of chairman–chief executive officer duality roles on a firm’s value: Evidence from the Thai listed firms. Global Business Review. Advance online publication. https://doi.org/10.1177/09721509221119705

Burkart, M., Panunzi, F., & Shleifer, A. (2003). Family firms. The Journal of Finance, 58(5), 2167–2201.

Carsrud, A. L., & Brännback, M. (2012). Understanding family businesses: Undiscovered approaches, unique perspectives, and neglected topics. Springer. https://doi.org/10.1007/978-1-4614-0911-3

Chen, S., Chen, X., & Cheng, Q. (2008). Do family firms provide more or less voluntary disclosure? Journal of Accounting Research, 46(3), 499–536. https://doi.org/10.1111/j.1475-679X.2008.00288.x

Chua, J. H., Chrisman, J. J., & Sharma, P. (1999). Defining the family business by behavior. Entrepreneurship Theory and Practice, 23(4), 19–39. https://doi.org/10.1177/104225879902300402

Claessens, S., Djankov, S., & Lang, L. H. P. (2000). The separation of ownership and control in East Asian corporations. Journal of Financial Economics, 58(1–2), 81–112. https://doi.org/10.1016/s0304-405x(00)00067-2

Cucculelli, M., & Micucci, G. (2008). Family succession and firm performance: Evidence from Italian family firms. Journal of Corporate Finance, 14(1), 17–31. https://doi.org/10.1016/j.jcorpfin.2007.11.001

Daily, C. M., & Dollinger, M. J. (1992). Empirical examination of family business. Family Business Review, 5(2), 117–136.

DeAngelo, H., & DeAngelo, L. (2000). Controlling stockholders and the disciplinary role of corporate payout policy: A study of the Times Mirror Company. Journal of Financial Economics, 56(2), 153–207. https://doi.org/10.1016/S0304-405X(00)00039-8

De Bakker, F. G. A., Groenewegen, P., & Den Hond, F. (2005). A bibliometric analysis of 30 years of research and theory on corporate social responsibility and corporate social performance. Business and Society, 44(3), 283–317. https://doi.org/10.1177/0007650305278086

Debicki, B. J., Matherne, C. F., Kellermanns, F. W., & Chrisman, J. J. (2009). Family business research in the new millennium: An overview of the who, the where, the what, and the why. Family Business Review, 22(2), 151–166. https://doi.org/10.1177/0894486509333598

Dharmani, P., Das, S., & Prashar, S. (2021). A bibliometric analysis of creative industries: Current trends and future directions. Journal of Business Research, 135, 252–267. https://doi.org/10.1016/j.jbusres.2021.06.037

Donthu, N., Kumar, S., Mukherjee, D., Pandey, N., & Lim, W. M. (2021a). How to conduct a bibliometric analysis: An overview and guidelines. Journal of Business Research, 133, 285–296. https://doi.org/10.1016/j.jbusres.2021.04.070

Donthu, N., Kumar, S., & Pandey, N. (2021b). A retrospective evaluation of Marketing Intelligence and Planning: 1983–2019. Marketing Intelligence and Planning, 39(1), 48–73. https://doi.org/10.1108/MIP-02-2020-0066

Durieux, V., & Gevenois, P. A. (2010). Bibliometric indicators: Quality measurements of scientific publication. Radiology, 255(2), 342–351. https://doi.org/10.1148/radiol.09090626

Ehikioya, B. I. (2009). Corporate governance structure and firm performance in developing economies: Evidence from Nigeria. Corporate Governance: The International Journal of Business in Society, 9(3), 231–243.

Eugster, N., & Isakov, D. (2019). Founding family ownership, stock market returns, and agency problems. Journal of Banking and Finance, 107, 105600. https://doi.org/10.1016/j.jbankfin.2019.07.020

Fernández, Z., & Nieto, M. J. (2006). Impact of ownership on the international involvement of SMEs. Journal of International Business Studies, 37(3), 340–351.

Ferreira, J. J. M., Fernandes, C. I., & Kraus, S. (2019). Entrepreneurship research: Mapping intellectual structures and research trends. Review of Managerial Science, 13(1), 181–205. https://doi.org/10.1007/s11846-017-0242-3

Gedajlovic, E., Carney, M., Chrisman, J. J., & Kellermanns, F. W. (2012). The adolescence of family firm research: Taking stock and planning for the future. Journal of Management, 38(4), 1010–1037. https://doi.org/10.1177/0149206311429990

Gómez-Mejía, L. R., Haynes, K. T., Núñez-Nickel, M., Jacobson, K. J., & Moyano-Fuentes, J. (2007). Socioemotional wealth and business risks in family-controlled firms: Evidence from Spanish olive oil mills. Administrative Science Quarterly, 52(1), 106–137.

Hasan, M. S., Rahman, R. A., & Hossain, S. Z. (2014). Monitoring family performance: Family ownership and corporate governance structure in Bangladesh. Procedia - Social and Behavioral Sciences, 145, 103–109. https://doi.org/10.1016/j.sbspro.2014.06.016

Hiebl, M. R. W., Quinn, M., Craig, J. B., & Moores, K. (2018). Management control in family firms: A guest editorial. Journal of Management Control, 28(4), 377–381. https://doi.org/10.1007/s00187-018-0260-6

Howorth, C., & Kemp, M. (2019). Governance in family businesses: Evidence and implications. Report to the Institute for Family Business Research Foundation. IFB Research Foundation. https://www.ifb.org.uk/media/4133/governance-in-family-businesses-evidence-and-implications_web.pdf

James, H. S. (1999). Owner as manager, extended horizons and the family firm. International Journal of Phytoremediation, 21(1), 41–55. https://doi.org/10.1080/13571519984304

Jensen, M. C. (1986). Agency costs of free cash flow, corporate finance, and takeovers. The American Economic Review, 76(2), 323–329.

Jiang, Y., & Peng, M. W. (2011). Are family ownership and control in large firms good, bad, or irrelevant? Asia Pacific Journal of Management, 28(1), 15–39.

Kabbah de Castro, L. R., Aguilera, R. V., & Crespí-Cladera, R. (2017). Family firms and compliance: Reconciling the conflicting predictions within the socioemotional wealth perspective. Family Business Review, 30(2), 137–159.

Kaur, A., & Singh, B. (2018). Corporate reputation: Do board characteristics matter? Indian evidence. Indian Journal of Corporate Governance, 11(2), 122–134.

Koji, K., Adhikary, B. K., & Tram, L. (2020). Corporate governance and firm performance: A comparative analysis between listed family and non-family firms in Japan. Journal of Risk and Financial Management, 13(9), 215. https://doi.org/10.3390/jrfm13090215

Kowalewski, O., Talavera, O., & Stetsyuk, I. (2010). Influence of family involvement in management and ownership on firm performance: Evidence from Poland. Family Business Review, 23(1), 45–59.

Lane, S., Astrachan, J., Keyt, A., & McMillan, K. (2006). Guidelines for family business boards of directors. Family Business Review, 19(2), 147–167.

Lubatkin, M. H., Schulze, W. S., Ling, Y., & Dino, R. N. (2005). The effects of parental altruism on the governance of family-managed firms. Journal of Organizational Behavior, 26(3), 313–330.

Mandl, I. (2008). Overview of family business relevant issues (Issue 30). Austrian Institute for SME Research. https://docplayer.net/5004871-Overview-of-family-business-relevant-issues.html

Mani, Y., & Lakhal, L. (2015). Exploring the family effect on firm performance: The impact of internal social capital dimensions on family firm performance. International Journal of Entrepreneurial Behaviour and Research, 21(6), 898–917. https://doi.org/10.1108/IJEBR-06-2014-0100

Maseda, A., Iturralde, T., Cooper, S., & Aparicio, G. (2022). Mapping women's involvement in family firms: A review based on bibliographic coupling analysis. International Journal of Management Reviews, 24(2), 279–305.

Mas-Tur, A., Roig-Tierno, N., Sarin, S., Haon, C., Sego, T., Belkhouja, M., Porter, A., & Merigó, J. M. (2021). Co-citation, bibliographic coupling and leading authors, institutions and countries in the 50 years of Technological Forecasting and Social Change. Technological Forecasting and Social Change, 165, 120487. https://doi.org/10.1016/j.techfore.2020.120487

McConaughy, D. L., Matthews, C., & Fialko, A. S. (2001). Founding family controlled firms: Efficiency, risk, and value. Journal of Small Business Management, 39(1), 31–50.

McConaughy, D. L., & Walker, M. C. (1998). Founding family controlled firms: Efficiency and value. Review of Financial Economics, 7(1), 1–19.

Merigó, J. M., Mas-Tur, A., Roig-Tierno, N., & Ribeiro-Soriano, D. (2015). A bibliometric overview of the Journal of Business Research between 1973 and 2014. Journal of Business Research, 68(12), 2645–2653. https://doi.org/10.1016/j.jbusres.2015.04.006

Miller, D., & Le Breton-Miller, I. (2006). Family governance and firm performance: Agency, stewardship, and capabilities. Family Business Review, 19(1), 73–87.

Miller, D., Le Breton-Miller, I., Lester, R. H., & Cannella, A. A. (2007). Are family firms really superior performers? Journal of Corporate Finance, 13(5), 829–858. https://doi.org/10.1016/j.jcorpfin.2007.03.004

Minh Ha, N., Do, B. N., & Ngo, T. T. (2022). The impact of family ownership on firm performance: A study on Vietnam. Cogent Economics and Finance, 10(1). https://doi.org/10.1080/23322039.2022.2038417

Mohd, A., & Wi, N. (2003). Socioemotional wealth, family commitment and firm performance in private family owned businesses in Bangladesh [Thesis]. University of Malaya.

Moher, D., Liberati, A., Tetzlaff, J., & Altman, D. G. (2009). Academia and clinic annals of internal medicine preferred reporting items for systematic reviews and meta-analyses. Annals of Internal Medicine, 151(4), 264–269.

Morck, R., & Yeung, B. (2003). Agency problems in large family business groups. Entrepreneurship Theory and Practice, 27(4), 367–382.

OECD. (2019). Principles of corporate governance. https://www.oecd.org/daf/ca/corporategovernanceprinciples/1930657.pdf

Paul, J., & Criado, A. R. (2020). The art of writing literature review: What do we know and what do we need to know? International Business Review, 29(4), 101717. https://doi.org/10.1016/j.ibusrev.2020.101717

Pearson, A. W., Carr, J. C., & Shaw, J. C. (2008). Toward a theory of familiness: A social capital perspective. Entrepreneurship: Theory and Practice, 32(6), 949–969. https://doi.org/10.1111/j.1540-6520.2008.00265.x

Peng, M. W., & Jiang, Y. (2010). Institutions behind family ownership and control in large firms. Journal of Management Studies, 47(2), 253–273. https://doi.org/10.1111/j.1467-6486.2009.00890.x

Pieper, T. M. (2003). Corporate governance in family firms: A literature review [Working Paper Series]. INSEAD. https://flora.insead.edu/fichiersti_wp/inseadwp2003/2003-97.pdf

Ponomareva, Y., & Ahlberg, J. (2016). Bad governance of family firms: The adoption of good governance on the boards of directors in family firms. Ephemera: Theory and Politics in Organization, 16(1), 53–77.

Pritchard, A. (1969). Statistical bibliography or bibliometrics? Journal of Documentation, 25(4), 348–349.

Priya, A. (2021). Globalization of the family business - Public policies, innovation, firm growth and contribution in GDP. Journal of Entrepreneurship & Organization Management, 10(4), 20–22.

Rovelli, P., Ferasso, M., De Massis, A., & Kraus, S. (2022). Thirty years of research in family business journals: Status quo and future directions. Journal of Family Business Strategy, 13(3), 100422. https://doi.org/10.1016/j.jfbs.2021.100422

Salvato, C., & Melin, L. (2008). Creating value across generations in family-controlled businesses: The role of family social capital. Family Business Review, 21(3), 259–276. https://doi.org/10.1111/j.1741-6248.2008.00127.x

Sarbah, A., & Xiao, W. (2015). Good corporate governance structures: A must for family businesses. Open Journal of Business and Management, 3(1), Article 53295.

Shivani, M. V., Jain, P. K., & Yadav, S. S. (2017). Governance structure and accounting returns: Study of NIFTY500 corporates. Business Analyst, 37(2), 179–194.

Shleifer, A., & Vishny, R. W. (1986). Large shareholders and corporate control. Journal of Political Economy, 94(3, Part 1), 461–488.

Siebels, J. F., & zu Knyphausen-Aufseß, D. (2012). A review of theory in family business research: The implications for corporate governance. International Journal of Management Reviews, 14(3), 280–304.

Sobjak, R., de Souza, E. G., Bazzi, C. L., Opazo, M. A. U., Mercante, E., & Aikes Junior, J. (2023). Process improvement of selecting the best interpolator and its parameters to create thematic maps. Precision Agriculture, 1–36. http://doi.org/10.1007/s11119-023-09998-4

Srivastava, A., & Bhatia, S. (2022). Influence of family ownership and governance on performance: Evidence from India. Global Business Review, 23(5), 1135–1153. https://doi.org/10.1177/0972150919880711

Suess, J. (2014). Family governance–Literature review and the development of a conceptual model. Journal of Family Business Strategy, 5(2), 138–155.

van Essen, M., Carney, M., Gedajlovic, E. R., & Heugens, P. P. (2015). How does family control influence firm strategy and performance? A meta-analysis of US publicly listed firms. Corporate Governance: An International Review, 23(1), 3–24.

Vazquez, P., Carrera, A., & Cornejo, M. (2020). Corporate governance in the largest family firms in Latin America. Cross Cultural & Strategic Management, 27(2), 137–163.

Viana-Lora, A., & Nel-lo-Andreu, M. G. (2022). Bibliometric analysis of trends in COVID-19 and tourism. Humanities and Social Sciences Communications, 9(1), 1–8. https://doi.org/10.1057/s41599-022-01194-5

Villalonga, B., & Amit, R. (2006). How do family ownership, control and management affect firm value? Journal of Financial Economics, 80(2), 385–417. https://doi.org/10.1016/j.jfineco.2004.12.005

Wallin, J. A. (2005). Bibliometric methods: Pitfalls and possibilities. Basic and Clinical Pharmacology and Toxicology, 97(5), 261–275. https://doi.org/10.1111/j.1742-7843.2005.pto_139.x

Weinberg, B. H. (1974). Bibliographic coupling: A review. Information Storage and Retrieval, 10(5–6), 189–196. https://doi.org/10.1016/0020-0271(74)90058-8

Zattoni, A. (2011). Who should control a corporation? Toward a contingency stakeholder model for allocating ownership rights. Journal of Business Ethics, 103(2), 255–274.

Zupic, I., & ?ater, T. (2015). Bibliometric methods in management and organization.

Organizational Research Methods, 18(3), 429–472. https://doi.org/10.1177/1094428114562629